Letter to the President of the Republic – France and Europe: from crisis management to a longer-term ambition

Letter submitted to

the President of the French Republic,

the President of the Senate and

the President of the National Assembly

by François Villeroy de Galhau, Governor of the Banque de France

This Letter comes at a special moment: 25 years of Monetary Union and the European elections this year. Furthermore, we are gradually emerging from the inflationary crisis that has affected our economies and fellow citizens since the Russian invasion of Ukraine, and we are again faced with the fundamental challenges of European growth.

Summary

Firstly, this is an opportunity to shed some light on the reasons behind the recent successes in curbing inflation, which has already come down to 2.4% in March, both in France and the euro area. The reversal of the initial supply shocks, affecting energy and food prices, has naturally helped a great deal. But monetary policy has also played a significant part, by limiting the spread to core inflation, excluding energy and food, which has fallen to 2.9% in the euro area and 2.2% in France, half the peak reached a year ago. By keeping the inflation expectations of households and businesses sufficiently well anchored, the credible action of central banks has prevented the formation of price-wage-margin spirals: this explains why this inflationary episode looks set to be much shorter than that of the 1970s, and its resolution less costly in terms of activity. The last few quarters have seen a real slowdown, but not a recession, and the chances of a soft landing are even greater now that the ECB is expected to rapidly begin cutting interest rates. Barring any new geopolitical shocks, 2025 should see inflation come back to 2% and a recovery in growth, both in France and in Europe. Moreover, Europe has got through the pandemic and then the sharp rate rise without experiencing a financial crisis this time, or a banking crisis such as the one that threatened the United States and Switzerland in March 2023: this is the positive effect of the strong tightening of regulation and supervision over the past ten years.

From a longer-term perspective, public support for the euro has grown steadily over the last 25 years, from 68% to 79% today. The euro has been particularly beneficial for the French, with inflation kept under a tighter rein, purchasing power rising significantly more than the European average (cumulative increase of 26% compared with 17% for Europe), and the cost of borrowing falling particularly sharply – for households and businesses as well as the state. But the euro is no substitute for tackling the pre-existing structural weaknesses in the French economy that explain our relative lag in growth: among these, we have made good progress over the last ten years on employment, but not on public finances.

Taking an even broader perspective, we can compare the euro area with the United States: the cumulative growth differential since 1999 is significant, even when adjusted for demographic changes (GDP per capita): 25% compared with 38%. It has a primary, “Schumpeterian” cause: innovation. The European economy has almost the same mass as the United States, but nowhere near the same speed. This means that we need to achieve three transformations for the future: the transformation of work, to complete the progress towards full employment but also to prepare for the decline in the working population in the future; the digital transformation and that of artificial intelligence; and of course the climate transition.

While there is consensus among Europeans on these common challenges and on our social and environmental model, there is often a feeling of powerlessness when it comes to finding solutions. This does not have to be the case. In a more fragmented, tougher world, European economic sovereignty requires a combination of three shared levers: size, multiplied by financial strength, multiplied by public efficiency.

Size means deepening the single market, with the aim of making it as attractive as the US market. There is still too much friction and too many internal borders, particularly in digital technology and services, and too much national state aid. Great Britain has lost 3 to 5 percentage points of GDP growth due to its departure from the existing single market; conversely, Europe could gain several percentage points of growth, particularly by following the recommendations of the report just submitted by Enrico Letta.

Financial strength means mobilising Europe’s private savings surplus – more than EUR 300 billion a year – to finance a large share of green and digital investment. To do this, we need to beef up the Capital Markets Union to create a genuine “Savings and Investments Union”, based notably on green securitisation and European venture capital.

Lastly, public efficiency naturally means keeping deficits and public debt under control, and, to this end, fostering greater efficiency in all central, local and social spending. Fiscal consolidation is first and foremost an imperative for France: hoping that the upward drift in spending can be resolved merely with a future acceleration in growth is an illusion that has been entertained for too long. But all of Europe needs to recreate the headroom to finance the necessary additional spending (climate, defence, population ageing), and spending on the future to generate potential growth (innovation and education). On this condition, the creation of a common fiscal capacity would be an additional asset for Europeans.

France and Europe today have doubts about their economic future. But self-flagellation and “every man for himself” do nothing to promote economic growth. Europe has great assets, first and foremost manpower and intelligence. And, as in the case of the euro, the potential to act as one. To paraphrase Raymond Aron, we can believe in the success of the European economy, but on one condition: that we have the will to be successful.1

1 In 1939, Raymond Aron wrote: “I also believe in the final victory of democracies, but on one condition, that they want to be victorious”.

1. Monetary union has been effective in tackling the inflationary crisis

Europe succeeded in responding effectively to a series of unprecedented shocks in recent years. First in 2020, when the pandemic threatened to bring the economy to a standstill and trigger deflation. Conversely, in 2022, the Russian attack on Ukraine and the resulting energy crisis led to a surge in inflation, which is in the process of being reined in thanks in particular to the European Central Bank’s monetary policy action (1).

But Europe must not be shaped solely by crises. The 25th anniversary of Monetary Union on 1 January this year and the forthcoming European elections call for a longer-term and broader assessment of the French economy in Europe and of the European economy relative to the United States. As the inflationary crisis comes to an end, we need to face up to our common structural challenges, and achieve three transformations: work, digital and climate (2).

Europe has the resources to succeed if, and only if, it acts as one. In view of the European lag and the growing geopolitical tensions, this Letter proposes three levers for Europe’s economic reawakening, in order to deliver on the promise of sustainable prosperity. It is time to mobilise our common assets confidently and decisively: we need to multiply size – a single market geared to the 21st century – by financial strength – a Financing Union for the Transition – and by improved public efficiency (3).

In recent years, France and Europe have experienced a period of high inflation. Inflation remains one of the primary concerns of French and, more broadly, European citizens.1 But barring any new shocks, France and the euro area should be able to achieve a “soft landing”, i.e.disinflation without recession.

1.1 Clear successes in the battle against inflation

The decline in inflation

After a strong resurgence from 2021 onwards, inflation has now fallen markedly. It peaked at 10.6% in October 2022 for the euro area and at 7.3% in February 2023 for France,2 and has since receded to 2.4% in the euro area and France in March 2024 (see Chart 1).3

Chart 1. Headline and core inflation in France and the euro area (%, year-on-year)

With cumulative inflation slightly below the European average and that of Germany (see Chart 2), France has followed a hump-shaped inflation path that is lower than the euro area peak.4 This is the result of specific pricing policies that were introduced early on and efficiently, and can therefore be phased out. The state can temporarily cushion shocks, but it cannot make them disappear.

Chart 2. Euro area consumer price index (December 2021 = 100)

The decline in inflation is obviously good news, even though it still remains too high. Barring any unexpected shocks, it is set to continue coming down over the next few months. According to our projections for France,5 inflation should fall to an annual average of 2.5% in 2024 and 1.7% in 2025. The Banque de France is therefore reiterating the commitment it made over a year ago: we are going to bring inflation down to 2% by 2025 at the latest.

However, apart from a few possible exceptions, prices will not fall back to their previous level: disinflation, i.e. the slowing of the rate of price increases, does not mean deflation and falling prices; such deflation would be a sign of a pronounced economic slump, or even a recession. Furthermore, income – including wages and pensions – has also risen, and will similarly not decline to previous levels.

Monetary policy has prevented the spread and persistence of inflation

Inflation was initially fuelled by shocks to energy and commodity prices, and these were therefore the initial drivers of disinflation when these shocks reversed (see Chart 3). In France, energy inflation, which reached an annual average of 23.8% in 2022, slowed sharply to 5.7% in 2023 and 3.2% in March 2024. However, it may still be affected by the return of normal rises in regulated electricity tariffs and by geopolitical tensions. Food prices are also continuing to slow in line with the gradual easing in international prices: after peaking at 15% in March 2023 in France, food inflation fell to 2.7% in March 2024, a trend that is set to continue in 2024.

Chart 3. Inflation and its components in France (%, year-on-year; components in percentage points)

But monetary policy is also playing its part in this disinflationary trend, by limiting the spread of these shocks to inflation excluding energy and food (i.e. manufactured goods and services prices).6 This component, which represents just over 70% of the consumption basket, was in danger of becoming more persistent and self sustaining.7 The European Central Bank (ECB) therefore raised rates at an unprecedented pace, by 450 basis points between July 2022 and September 2023 (see Chart 4).

Chart 4. Key interest rates in the euro area and the United States

As a result,core inflation, excluding energy and food, passed its peak in the spring of 2023, and fell to 2.9% in the euro area and 2.2% in France in March 2024. This decline reflects the particularly sharp slowdown in manufactured goods prices (from a peak inflation rate of 5.6% year-on-year in March 2023 to 0.4% in March 2024 for France), while services prices, which are traditionally stickier, are slowing more gradually (3.2% inflation in March 2024 compared with 4.0% a year earlier) and should continue to ease in 2025 and 2026.

The impact of monetary policy was first transmitted through the traditional credit channel, which dampened demand at a time when supply was becoming increasingly constrained (energy price shocks, disruptions to global supply chains). But the fact that disinflation has occurred without a recession (see section 1.2) can largely be ascribed to a second transmission channel, that of inflation expectations : the high credibility of central banks has made it possible to “anchor” price-and wage-setting behaviour, and avoid a wage-price spiral such as that seen in the 1970s. The overall impact of monetary policy is estimated to have avoided 1 to 2 percentage points of inflation in 2023,8, 9 with an even greater impact in 2024 and 2025 due to the time lag in the transmission of monetary policy.

To reach our target of 2% by 2025 at the latest, there is still a “last mile” to go. This last mile will probably be a little slower than the previous ones – services disinflation may be more gradual – but it should not be any more arduous. On the other hand, we must not ignore the risk that, by keeping our foot on the monetary brake for too long, we could weigh excessively on activity. This is why the time has come to start cutting rates, which should start in early June.

Now that the question of the initial timeframe has largely been decided upon, two other issues need to be addressed: the pace of rate cuts thereafter, and the “landing zone” for interest rates. For this, we should adopt a policy of pragmatic and agile gradualism: pragmatic, meaning data-driven. And agile, because we have significant room for manoeuvre before monetary policy becomes too accommodative again, without returning to the zero or ultra-low interest rates of the previous era. Indeed, the neutral rate or equilibrium rate R* currently seems to be around 2% to 2.5% in nominal terms in the euro area.

There are still geopolitical risks, of course, starting with the conflict in the Middle East. If the escalation were to trigger a sharp rise in oil prices, the Eurosystem would have to carefully examine the consequences for the inflation outlook. They could be limited in light of three criteria: the potentially temporary nature of the shock; whether or not it spreads to inflation expectations and core inflation; and its restrictive impact on activity. However, if the inflationary effect were to prove more significant, we would have the capacity, after the first rate cut, to adjust the pace of our next moves as needed: monetary policy will indeed remain in restrictive territory for some time.

1.2 Towards a soft landing

Alongside the cycle of monetary tightening, economic activity has undeniably slowed, but has not yet turned around: in France and the euro area, we have avoided a recession scenario, with growth of 0.9% and 0.5% respectively in 2023, and forecasts for 2024 of 0.8% and 0.6% (see Chart 5). Driven mainly by household consumption on the back of falling inflation, economic activity is expected to accelerate significantly in 2025 and 2026.

Chart 5. GDP growth in France and the euro area (annual average % change)

Temporary contraction in investment

In the short term, the rise in interest rates is undoubtedly curbing household investment (-5.1% in 2023, -4.3% in 2024), after several years of very strong growth since 2015. This mainly concerns real estate investment, which is reflected in new housing loans (EUR 7.3 billion in February). The problem is now essentially one of demand and a wait-and-see attitude on the part of households, which should gradually subside as property prices begin to fall. On the supply side, lending rates are tending to stabilise and even fell slightly in February, reflecting the stabilisation of ECB rates and the fall already seen in long-term market rates. Furthermore, the increase in flexibility margins decided by the Haut Conseil de stabilité financière (HCSF – High Council for Financial Stability),10 which are still far from being fully taken up, has resolved this issue.

It would therefore be pointless and potentially dangerous to call into question the French mechanism for financial stability, which has proven its worth since the creation of the HCSF in 2013. Despite an almost twofold rise in the household debt ratio in the past 20 years (see section 2.1), housing loans remain very secure, to the benefit of borrowers and lenders alike. It is therefore important to preserve the French financing model, based on very low rates, low margins and very secure credit. This need for continuity also applies more broadly to progress on regulation (Basel III for banks) and on supervision, which has been unified over the past ten years: this time round they protected Europe effectively from the risk of a financial crisis, throughout the pandemic and the sharp rise in interest rates, whereas the United States

and Switzerland were threatened with a banking crisis in March 2023.

Regarding businesses, investment is expected to contract by a more modest 0.6% in 2024, and then to gradually recover, thanks in particular to the stability of profit margins and decreasing interest rates. For both businesses and households, investment in 2024 is expected to remain well above its 2015 level (+28% and +7% respectively).

In average terms, employment and purchasing power are holding up better

Employment showed remarkable resilience in 2023 thanks to the successful French labour market reforms, even if it has begun to temporarily lose steam as a result of the slowdown in activity. The unemployment rate is rising due to cyclical factors, from its low of 7.1% in the first quarter of 2023 to 7.5% in the fourth quarter of 2023. It should continue to pick up slightly, reaching 7.8% in 2025 – well below the 2013 peak (10.5% in the second quarter of 2013) – before starting to fall back as of 2026.

Nominal wages, meanwhile, are catching up with inflation, and have on average begun to outpace it since the start of 2024 (see Chart 6). Real wages should therefore start to rise again in 202411 as inflation recedes.

Chart 6. Average per capita wage in the market sector and inflation in France (year-on-year % change, quarterly data)

Despite the episode of high inflation, per capita purchasing power was broadly preserved in 2022 and 2023 (-0.1% and +0.5% respectively, see Chart 7). In 2023, however, this figure masked a decline in real wages, which was offset by continued buoyant job creation and the high level of social transfers and benefits, and even more so by the rise in income from wealth (more concentrated within the population). The expected rise in real wages in 2024 should bolster purchasing power, while ensuring a wider distribution of the gains.

Chart 7. Purchasing power per capita in France (annual average % change)

Inflation has had a bigger impact on our most vulnerable fellow citizens and those living outside our main cities. As part of its services to the economy and society, the Banque de France is more attentive than ever to these households. We will continue to monitor closely the changes in banking incidents and overindebtedness applications, which increased by 8% between 2022 and 2023 but remain lower than in 2019 (the pre-Covid reference year).12

2. Beyond the crisis, taking a broader view of the European economy

Europe has just passed a milestone with the 25th anniversary of the euro13 – now the single currency of 20 countries compared with 11 at its introduction on 1 January 1999. Today, the euro enjoys historically high levels of trust among its 350 million or so European users. In the autumn of 2023, 77% of French people and 79% of Europeans said they supported the euro (see Chart 8).14 This trust has grown significantly over the past 25 years.

Chart 8. Public support for the euro

The public’s trust can be attributed to the fact that inflation has been kept in check over the long run (average of 2.1% per year), and to the Eurosystem’s credibility – which has been bolstered by its sound management of the crises. This 25-year milestone is also an ideal opportunity to conduct a long-term appraisal from two angles: first looking at the French economy within Europe, and then at the European economy relative to the United States.

2.1 The French economy in Europe

The French economy’s relative position, over the course of six different parliamentary cycles and majorities, is marked by three paradoxes that are relatively permanent and hence structural.

Stronger gains in purchasing power, but lower GDP growth

It may come as a surprise given the perceptions of our fellow citizens, but the purchasing power of disposable income per capita has in fact risen markedly in France, by a cumulative 26% since 1999, compared with just 17% for the euro area as a whole (see Chart 9). This growth has been driven by higher social transfers – and therefore public deficits – than in neighbouring countries, as well as by robust real wage growth.

Chart 9. Purchasing power per capita in the euro area (1999 = 100)

By contrast, GDP per capita has risen more slowly in France, expanding by a cumulative 19% between 1999 and 2023 compared with 25% growth in the euro area as a whole (see Chart 10a).

Chart 10. GDP per capita in the euro area

a) Cumulative change (1999 = 100)

France initially lagged behind Germany in terms of growth, but since 2015 has outstripped it again (see Chart 10b), especially in 2023 (+0.9% in France compared with -0.1% in Germany). However, Italy and Spain have done substantially better since 2015, recouping the ground lost after the financial crisis. The worst performer overall is Italy. France’s lower cumulative growth is attributable to smaller contributions from employment and productivity than in the rest of the euro area.15

Chart 10. GDP per capita in the euro area (continued)

b) Change per period (annual average % change)

Inflation slightly below the euro area average, but some erosion of competitiveness

With the introduction of the euro, inflation in both France and the euro area more than halved compared with the preceding period (1980-98, when it averaged 4.3%). Inflation averaged 2.1% in the euro area from 1999 to 2023, which is very close to the target of 2% over the medium term (see Chart 11). It was slightly lower in France in annual average terms, at 1.9%, resulting in a fairly large cumulative difference over the 25-year period: as a result, from 1999 to 2023, the general price level rose faster in the euro area (+68%) than in France (+57%).

Chart 11. Inflation rate in the euro area (%, annual average per period)

With inflation running below the euro area average, France might have expected a boost in its relative competitiveness. Yet the French economy’s export performance (i.e. its ability to meet foreign customers’ demand) deteriorated over the period (see Chart 12).

Chart 12. Export performance per country (%, annual average per period)

Although its cost-competitiveness (as measured by unit labour costs) remained in line with the euro area average – after dropping behind Germany in the first decade (see Chart 13) – its non-cost competitiveness is still lagging today. This structural problem appears to be linked in particular to a weakening of France’s industrial base and to insufficient upskilling.

Chart 13. Unit labour costs in the euro area (1999 = 100)

Borrowing on more favourable terms, but bigger deficits

French borrowers (households and businesses alike) have benefited more than most from the lower interest rates stemming from the euro. Between 2003 and 2023, rates declined by an average of 4.8 percentage points for households and 1.6 percentage points for businesses (see Chart 14). In 2023, the average rate for French borrowers was well below the euro area average, and even below the German average. This is notably a testament to the efficiency of our banking system.

Chart 14. Average interest rate on loans in the euro area (%)

a) To households

b) To non-financial corporations

As a corollary of this, private debt in France has risen much faster than the euro area average and now stands well above it (see Chart 15); this observation is true for both households16 and businesses. This fact, which is often overlooked, is grounds for vigilance in terms of financial stability. But it also illustrates just how beneficial euro financing conditions have been for French economic players.

Chart 15. Private debt in the euro area – households and non-financial corporations (% of GDP)

The state – and hence the taxpayer – has also benefited from increasingly advantageous market interest rates, even with the rise seen since mid-2022 (see Chart 16). In 1980, it was borrowing at 13.8% for maturities of 10 years (4.6% in 1999), while in mid-April 2024 the 10-year rate was just 2.9%.

Chart 16. Long-term sovereign yields in France and Germany (%)

For a long time, these increasingly favourable financing conditions led to a gradual easing of the interest burden. Unfortunately, France failed to seize this opportunity to cut its debt, unlike other members of the euro area. Systematic deficits have led to a massive rise in our public debt: in 1980 it was just 20% of GDP; in 1999 it was still only 60%; but in 2023 it stood at 111% and has been falling too slowly since the Covid shock, leaving a gap of 20 percentage points between France and the euro area, and of around 50 percentage points between France and Germany (see Chart 17).

Chart 17. Public debt in the euro area (% of GDP)

The rise in rates since mid-2022 will now have a detrimental impact on French public debt. Whereas the interest burden was EUR 29 billion in 2020, it is now expected to reach around EUR 58 billion in 2024, which is more than the defence budget, and around EUR 80 billion in 2027,17 which is nearly as much as the education budget. The moment of truth has come for fiscal consolidation (see section 3.3).

At the same time, the external deficit has also widened. While Germany’s surplus may appear abnormally high,France’s current account balance has deteriorated since the start of the 2000s (see Chart 18) amid lacklustre export performances. Over the past two years, it has also been impacted by the rise in the cost of energy imports following Russia’s invasion of Ukraine. This imbalance reflects the French economy’s overall net borrowing position, as the high level of household savings is insufficient to offset the net borrowing of general government and, to a lesser extent, businesses.

Chart 18. Current account balances in the euro area (% of GDP)

To sum up, this assessment of France’s relative performance appears to be fairly characteristic. The euro has certainly helped the French, by keeping inflation under a tighter rein, allowing purchasing power to rise by significantly more than the euro area average, and enabling interest rates to fall particularly sharply – to the benefit of households and businesses as well as the state.

But the euro cannot solve all the French economy’s problems on its own. We have persistently put off dealing with the structural weaknesses that existed before the euro and which account for our relative lag in growth: insufficient employment, despite recent progress (see section 2.3), the need for upskilling, and the excessive size of our deficits and public debt. Put another way, we the French have collectively, and for far too long, opted for easy, short-term fixes – most often in the form of higher public expenditure and general debt – rather than genuine, longer-term solutions. In a competitive and rapidly changing world, the euro is definitely a help, but it is not a magic bullet. A lot of the progress needed still depends on us, the people of France, and our democratic choices... which is ultimately good news.

2.2 The European economy vis-à-vis the United States

Over the past 25 years, Europe has established itself as a major monetary and economic force on the international stage, but overall it lacks momentum. To tackle this, we need to refine our analysis of its growth. Euro area GDP has expanded by a cumulative 36% since 1999, compared with 65% for the United States and 57% for the OECD countries as a whole. The gap began to open up after the great financial crisis, which was immediately followed in Europe by the sovereign debt crisis. It has widened even further recently with Russia’s war in Ukraine, which has affected Europe much more directly than the United States.

This striking growth gap sometimes triggers alarm bells in Europe; however, it needs to be put into perspective. Since 1999, Europe has partially caught up in terms of employment (see section 2.3), which has compensated for its lower productivity growth (see Chart 19a).

Chart 19. GDP per capita in the euro area, United States and OECD

a) Change between 1999 and 2022, and components (annual average % change, percentage point contributions)

Moreover, when adjusted for demographics (higher population growth in the United States), the growth differential is smaller, albeit still significant (see Chart 19b): 0.9% per year on average between 1999 and 2023 in the euro area, compared with 1.3% in the United States, i.e. cumulative growth of 25% and 38% respectively.

b) Per period (annual average % change)

Three potential “culprits” are sometimes singled out to explain Europe’s long-term lag: our social model, our macroeconomic policies and our lack of innovation. The first two are said to indicate the limitations of policies inspired by Keynes. However, the contention that Keynesian policies have failed does not hold up to closer analysis: monetary and fiscal policies have been very accommodative in both Europe and the United States for at least the past decade, and the success of northern European countries is proof that the European social model is compatible with growth.

Schumpeter, the other great European economic thinker of the 20th century, focused on the causes of economic dynamism and innovation: Europe is undeniably lagging behind in these two areas, which explains why our labour productivity is less robust (+0.9% per year in the euro area between 1999 and 2022, compared with +1.6% in the United States over the same period). This is legitimately one of the central themes of a notable speech by Mario Draghi,18 ahead of his forthcoming report on European competitiveness.

In absolute terms, and measured at purchasing power parity, the European Union (EU) and United States have fairly similar levels of GDP (see Chart 20). But despite being almost equivalent in size to the US market, our European single market is less attractive and dynamic; this challenge, coupled with our much smaller financial firepower, deserves a special focus (see section 3.1).

Chart 20. Population, GDP and stock market capitalisation in Europe and the United States

Europe now needs to join together these two strands and reconcile Keynes with Schumpeter.19 To boost our growth and tackle our shared challenges, we need to achieve three great transformations.

2.3 Three transformations for the future: work, digital, climate

Successfully transforming work

The first transformation we need to complete is that of work. Employment has increased significantly in the euro area over the past 25 years, and has proved remarkably resilient since 2020 despite successive economic shocks (see section 1.2). The euro area employment rate exceeded 70% in 2023, which is only 2 percentage points below that of the United States, compared with a gap of 13 percentage points in 1999 (see Chart 21).

Chart 21. Employment rate in France, the euro area and the United States (% of working age population)

At the same time, the unemployment rate reached a historical low of 6.5% in the euro area at the end of 2023, and 7.5% in France, even though this is still higher than the US rate of 3.7% (see Chart 22).

Chart 22. Unemployment rate in France, the euro area and the United States (% of labour force)

With the impact of the past decade’s successful employment reforms,20 France is closer than ever to achieving full employment. The temporary rise in unemployment linked to economic conditions should not cause us to lose sight of this ambition, even though we are looking at a horizon of the end of the decade, and therefore beyond the next milestone of 2027. This goal would allow us to solve the most unacceptable economic – and above all social – paradox in our country: on the one hand, 39% of firms are having difficulty recruiting, while on the other 2.3 million people, including 600,000 young people, are out of work. Success here means winning the skills battle: we have made clear progress with apprenticeships for young people (400,000 jobs created since 2019); we now need to genuinely improve professional training for adults by stepping up the efforts already underway with the creation of France Compétences. And of course, continue reforming our education system.

In addition to these reforms in France, the transformation of work will increasingly involve common requirements for European countries. The first shift is psychological and managerial. It is wrong to assert that young people or Europeans in general “no longer want to work” after Covid; but we must admit that Covid has highlighted and amplified changes in motivation for work. The welcome adoption of teleworking, a strong demand for autonomy and professional mobility, as well as a real desire for a sense of purpose in work, are all potential levers.

The second shift today is the shortage of labour. Europe is directly confronted with ageing demographics: the tipping point, where the working-age population will start to decrease, is expected as early as 2024 in Germany, and around 2030 in France.21 This quantitative issue also raises qualitative questions, in particular about how women (and men) can reconcile work more effectively with other imperatives, building notably on research conducted by Nobel Prize-winner Claudia Goldin.22 More generally, the shortage of labour will place the focus more clearly on the issue of productivity, which leads us to the second transformation: innovation, and more specifically the digital transformation.

Accelerating our digital transformation

We need to close our technology gap with the United States – and now with China as well. This is illustrated by the number of information and communication technologyrelated patents filed, which was almost twice as high in the United States as in Europe over the period 2015-20.23 Obviously, all major Bigtechs are American or Chinese, not European. The same is true in terms of technology uptake: firms, especially SMEs, tend to have lower levels of digitalisation in comparison to the United States, and hence lower aggregate total factor productivity growth.

Ongoing technological innovations, and especially current developments in artificial intelligence (AI), are opening up new horizons.24 Many people have concerns about how generative AI will impact certain professions. Indeed, for certain tasks, AI is likely to enable capital to replace labour in the short term. But AI will boost productivity, which will bring down prices of goods and increase demand. Based on economic history, a cautious “techno optimistic” approach appears possible. This means simultaneously regulating and developing AI in Europe, rather than fearing it.

Maintaining Europe’s leadership in the climate transition

The third transformation – the climate and energy transition – is of course an imperative, not only in response to the proven threat of global warming, but also due to the harsh lessons drawn from our past dependence on Russian hydrocarbons. Europe needs low-carbon, independent and competitive energy sources. It has made firm commitments in this field, with a target of reaching net zero by 2050. A radical energy transition will imply major efforts to adapt on the part of economic agents, and the introduction of appropriate incentives. The difference of approach between Europe and the United States is particularly evident when it comes to the form these incentives should take: regulation (as in the case of Europe’s highly ambitious “green package”), subsidies (as with the US Inflation Reduction Act), or carbon pricing? The three points of this triangle are not necessarily incompatible; each has its limits, taken in isolation: fear of “punitive ecology” in the case of regulation; fiscal overshoots and political risks for subsidies; and strong social resistance to pricing.

The fact remains that the price of carbon will have to rise: although politically unpopular, it remains an economic no-brainer. Whatever form it takes,25 carbon pricing will have to be global – not just national or European – and socially equitable. Europe – which is ahead in this field – needs to press relentlessly for this international “new frontier”. Only a “price signal” will succeed in aligning the behaviour of firms, consumers and private finance, by making yields on green investments attractive. Yet in 2022, only 22% of global emissions were covered by a carbon pricing mechanism. In Europe, the carbon trading system (EU ETS) covers around 40% of total EU emissions and, since its introduction in 2005, emissions in those sectors concerned (electricity, energyintensive industries, etc.) have fallen by 41%. The reform adopted in 2023, which will extend the scheme to other sectors (air, road and sea transportation, construction, fuel), should lead to a rise in the carbon price by 2030 and to a further fall in emissions.

3. Towards European economic sovereignty

As regards the challenges, there appears to be a consensus among Europeans. But when it comes to solutions, a sense of powerlessness looms, as Europe is constrained by overly national priorities and an agenda that is too short term. This European torpor is all the more irksome in the face of American speed and Chinese assertiveness.

This situation is by no means inevitable. From the end of the 19th century, Europe built a unique political narrative, reconciling economic growth and social justice with a pioneering “European social model”. The European narrative in the 21st century – a rallying point for our fellow citizens as well as for the rest of the world – should focus on how to combine prosperity and sustainability, growth and ecology. It should also be about increasing our strategic autonomy in a more fragmented world beset by geopolitical tensions. Aside from the semantic debates, we can argue for European economic sovereignty while rejecting protectionism. Putting the brakes on international trade, as too many American election manifestos are unfortunately seeking to do, is a losing proposition for everyone. The following guidelines are all about beefing up Europe’s economy.

Three levers for action need to be combined to fully unlock Europe’s potential: leveraging our size through the single market; aligning our financial strength with our economic heft through a genuine Financing Union; and enhancing the effectiveness of public action through a medium-term fiscal strategy.

3.1 Size: the single market

The single market is often seen as a thing of the past, the glorious economic legacy of Jacques Delors, whose genius was to collect together some 300 pieces of technical legislation under the banner of the four freedoms of movement, i.e. goods, services, people and capital. On the contrary, the single market is clearly a subject for the future. We should refer here to the report just submitted by former Italian Prime Minister Enrico Letta and his proposals for the energy, telecoms, defence and financial sectors.26 He also proposes the introduction of a “fifth freedom”, focusing on research, innovation, knowledge and education. The EU is now one of the largest markets in the world. The current single market has already boosted European GDP by between 8% and 9%, according to firm estimates from the European Commission.27 These estimates sometimes give rise to a certain amount of doubt, but the very real example of the British economy illustrates “by absurdity” the economic losses related to the absence of a single market.

But the full potential of the single market is far from having been unlocked. Recent academic research shows that the gains from integration are uneven between different sectors of activity and countries.28 In particular, it highlights the significant barriers that remain within the single market, creating “border effects”, even between adjacent regions (between France and Spain, for example).29 The IMF estimates that a 10% reduction in internal barriers and frictions would generate significant gains, in the order of 7% of GDP,30 for the benefit of all EU countries. Conversely, a counterfactual scenario consisting of replacing the single market with a simple free trade agreement, would cost the EU’s founding Member States between 3% and 5% of GDP.31

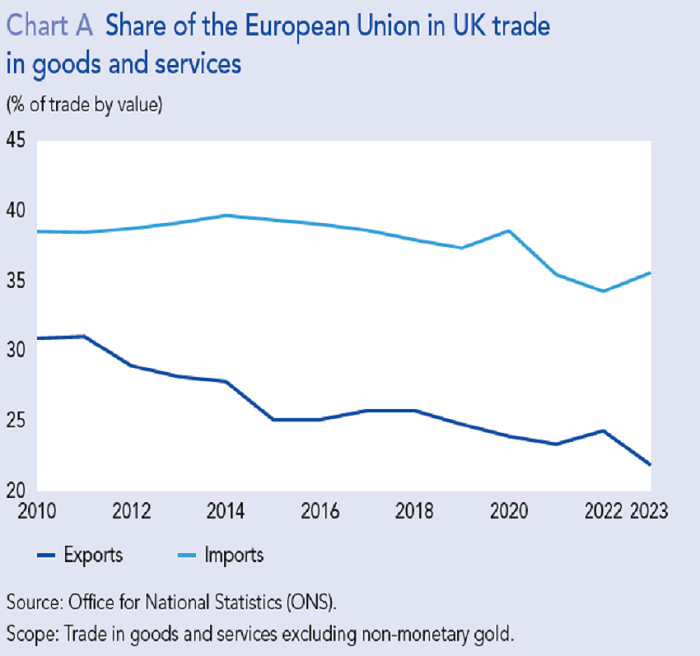

The economic costs of Brexit

The United Kingdom’s exit from the European Union (EU), voted in June 2016 and effective from 1 January 2021, provides an interesting empirical example of the costs associated in particular with loss of access to the single market. Just over three years after the effective date, the economic costs of Brexit are already estimated by the United Kingdom’s own analysts at between 2% and 3% of UK GDP, and they could rise to 5% or 6% of GDP by 2035.1

The reappearance of trade barriers with the EU is one of the key explanatory factors. The decline in trade flows with the EU has been significant since 2016, due to the increase in both customs tariffs and non-tariff barriers, generating an increase in the United Kingdom’s trade deficit (see Chart A).

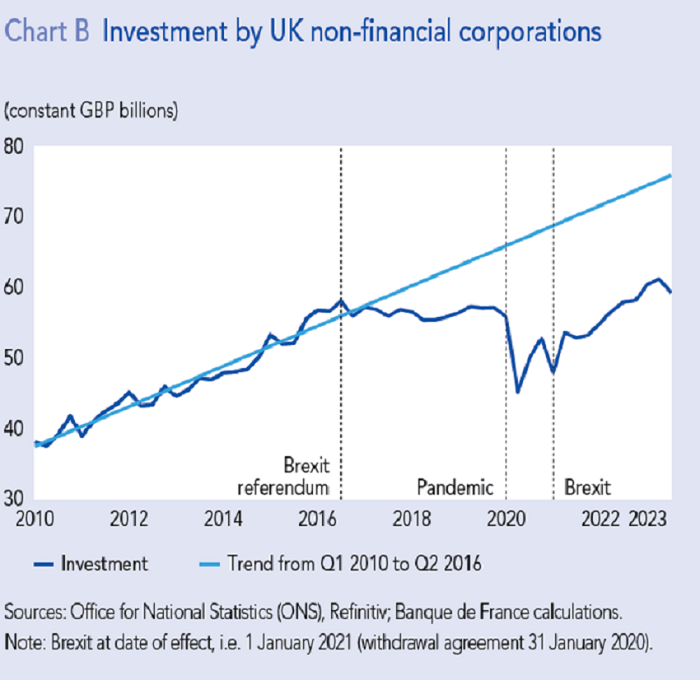

Exiting the single market and the uncertainty this creates,2 explain in large part the very sharp drop in business investment in the United Kingdom, estimated at between 10% and 20% relative to the pre-Brexit trend (see Chart B).3

Moreover, the necessary reorganisation of value chains, obstacles to the movement of people and sub-optimal allocation of production factors are negatively impacting the United Kingdom’sproductivity and potential growth.

1 National Institute of Economic and Social Research (NIESR) (2023), “Revisiting the effect of Brexit”, NiGEM Topical Feature, autumn.

2 See also IMF (2023), “2023 Article IV Consultation with the United Kingdom”, IMF Country Report, No. 23/252, July, and “United Kingdom: Selected Issues”, IMF Country Report, No. 23/253, July, on the effects of Brexit-related uncertainty on business investment.

3 See also Bank of England (2021), “Influences on investment by UK businesses: evidence from the Decision Maker Panel”, Quarterly Bulletin, 2nd quarter, June, and Haskel (J.) and Martin (J.) (2023), “How has Brexit affected business investment in the UK?”, March.

Digital technology and industrial innovation

In particular, we need to aim for a single digital market that combines talent development, regulation and financing. Achieving pan-European scale must be an important first step for our digital service players, before they establish themselves as global champions.

Here, there is a major need for training at European level: there were only 9.4 million digital specialists in the EU in 2022, still well short of the EU target of 20 million by 2030.32 In terms of regulation, a single digital market also requires greater intra-European interoperability and greater visibility over standards and guidelines in order to remove one of the main obstacles to IT investment cited by businesses (particularly SMEs).33 The Commission has begun to move in this direction, rounding out its pioneering regulatory initiatives to guarantee a secure, fair and open online environment.34 Moreover, the proposed idea of a “European Artificial Intelligence Community” could foster the emergence of European players.35

A deeper single market would also help leverage the EU’s unique blend of innovation and manufacturing strengths.The EU should not break ranks; nevertheless, there has been a plethora of national measures recently – to attract, for example, non-European manufacturers of electric vehicles or batteries. These risk undermining a fair and optimal allocation of investments: they should not go to areas where governments are more able and willing to provide (very costly) state aid, but should ensure the best use of economic resources.36 We therefore need to reintroduce better controls over national state aid within the EU, and maybe use some of the resulting savings to develop a European fiscal capacity: the Letta report proposes that states that want to grant national aid should allocate a portion of it to financing pan-European financing initiatives and investments.

We also need to channel our energies towards a truly European industrial policy focused on the sectors of the future – as is beginning to happen in semiconductors, for example. This industrial policy must be underpinned by public-private partnerships, increased investment in crossborder infrastructure, and enhanced European procedures for screening foreign investment.37 To achieve this, European competition policy needs to be more strategically oriented.

Services

Significant non-tariff barriers remain, especially in services, which have taken over from goods as drivers of international trade growth (see Chart 23). France has expertise and powerful companies in the services sector – and therefore a comparative advantage. Since the creation of the Monetary Union, France has largely diversified its positioning beyond tourism, and business services now account for the bulk of its exports38 – we should mention the increasing share of financial services in France’s balance of trade, a reflection of the attractiveness of Paris as a financial centre since Brexit.

Chart 23. Comparison of changes in GDP and trade in goods and services in France (current prices, 2000 = 100)

The fourth freedom of Jacques Delors’ single market, that of free movement of capital, is especially important today if we are to successfully achieve our future climate and digital transformations. Conventional wisdom states that these transformations are desirable but impossible to finance. And yet they can be financed – subject to one essential prerequisite: the private sector must shoulder the bulk of the necessary investment. And that means that Europe must finally realise its potential in terms of its financial strength.

3.2 Financial strength: a Savings and Investments Union to support the transition

To unleash our full financial potential, we need to revise our ambitions significantly upwards, by aiming higher and enhancing our instruments.39

Rallying around a higher and better purpose

For the past ten years, the Capital Markets Union (CMU) has been promoted mainly for its stabilising effect and to cushion asymmetric shocks, two objectives that have had an insufficiently galvanising effect from a political standpoint. A window of opportunity recently opened with Christine Lagarde’s call for a “Kantian shift” in our approach to the CMU, 40 followed by the unanimous position of the Eurosystem Governing Council on 7 March, 41 and the declaration of the European Council on 22 March 2024.42 In France, the Minister of the Economy and Finance has also entrusted Christian Noyer with the task of coming up with “concrete recommendations” in this area.

The objective of the CMU is today very clear: it must enable us to unlock the funding needed for Europe’s dual transformation – ecological and digital – with a view to allocation. And to underline this purpose, rebranding it would be highly desirable: a Savings and Investments Union, as notably proposed by the Letta report, or a Financing Union for Transition. At EU level, the green transition will require up to EUR 620 billion of additional funding per year through to 2030 (or 3.7% of EU GDP in 2023), according to the Commission,43 and 2.6% of GDP according to the I4CE44 (see Chart 24).

Chart 24. Some estimates of the amount of financing needed for the environmental transition (% of 2023 current GDP)

Added to this are another EUR 125 billion for the digital transition. Europe must tap into the “unknown resource” of its vast savings surplus to finance them: in the face of large public deficits, Europe’s private savings surplus (businesses and households combined) represented over 4% of EU GDP in 2023 (see Chart 25). All in all, after deducting public deficits, the EU’s net lending position amounts to almost 2% of GDP, and more than EUR 300 billion. This is currently the annual outward flow of European savings invested in the rest of the world.

Chart 25. European Union’s net lending position (% of GDP)

This Savings and Investments Union must incorporate the fundamental – and older – project of a Banking Union, which remains a partial success, i.e. effective completion of a “Supervisory Union” created ten years ago, but absence of any real cross-border European banks comparable in scale to their American competitors. Together, pan European banks and capital markets would constitute a powerful vector enabling savings to circulate more effectively throughout Europe.

Enhancing our levers with more ambitious instruments for innovation

Aside from continuing the work already carried out on a number of issues such as the harmonisation of insolvency law,45 four ambitious instruments need to be deployed.

Equity financing

In Europe, equity financing lags far behind the United States: in the third quarter of 2023, it only represented 84% of euro area GDP, versus 173% in the United States (see Chart 26).

Chart 26. Non-financial corporation liabilities (% of GDP in Q3 2023)

Europe and France are not short of credit, they are short of equity.46

Developing equity financing is particularly crucial for innovation, given the higher degree of risk involved and the need for long-term financing. There is undoubtedly growing momentum in this area; however, the European venture capital fund that has raised the most money over the last five years – which happens to be Swedish, and therefore outside the euro area – is still smaller than the tenth largest American venture capital fund (see Chart 27).

Chart 27. Amounts raised by the ten largest venture capital funds between 2019 and 2023 in the United States and Europe (EUR billions)

We probably still need to identify and remove the legal and tax obstacles to “European-scale” – and therefore genuinely cross-border funds, both in terms of their investors and their investments. But these long-term projects need to be rounded out by an ambitious public-private partnership that amplifies and standardises existing arrangements around the European Investment Bank.47 Such a partnership could use a system of labelling based on criteria of geographical diversification and sectoral prioritisation, opening up the possibility of public funding, allocated on a pari passu basis and for significantly higher amounts (at least EUR 10 billion to EUR 20 billion). At the same time, European savings products could be developed that go beyond the revised regulatory framework for European Long-Term Investment Funds (ELTIF).

Green finance and securitisation

Green finance clearly provides a fast track to a Financing Union. Europe is a pioneer in this area. It has adopted a single rulebook (Taxonomy, SFDR, CSDR)48 and is a major issuer of green bonds, accounting for 40% of the global market in 2023. However, it is lagging far behind in green securitisation – 90% of which is issued in the United States – even though this represents a massive potential source of financing for the transition. At the end of 2023, European regulations opened up the possibility of using the European Green Bond label (EuGB) for green securitisations, provided that the funds unlocked from bank balance sheets – for example by securitising housing loans – are allocated to European Taxonomy-aligned sustainable activities. To support the development of this market segment, these arrangements could be rounded out by the creation of a common European issuance platform, or even by public incentives such as a European guarantee. This could boost banks’ capacity to finance green projects by several hundred billion euro a year.

The technological leap in infrastructures and market operations

The Eurosystem has made a big contribution to the integration of European markets through its infrastructures, but it again has an important role to play in harnessing all of the benefits of technologies that have recently emerged in the financial sector. Distributed ledger technologies (DLT or blockchain) and tokenisation of financial instruments offer intrinsic advantages including speed, security and low transaction costs. Various initiatives have been launched by the private sector but they remain fragmented and limited in scale. They also face serious limitations, including a risk of fragmentation and the fact that settlement in stablecoins offers players much less security than central bank money.

A European unified ledger, involving the Eurosystem and commercial banks along with shared governance and standards, would remove these obstacles. Final settlement would take place in wholesale central bank digital currency (CBDC), which – alongside a “retail digital euro” – is the focus of exploratory work by the Eurosystem, supported by pioneering experiments conducted by the Banque de France since 2020. This unified ledger could eventually be used to record all types of “tokenised” assets, beginning with those segments where the need for efficiency is most acute (e.g. the capital of unlisted companies or the distribution of investment funds). Such an infrastructure would reduce transaction costs as well as counterparty and operational risks, and facilitate the provision of seamlessly connected services across Europe. It would therefore act as a catalyst for the Financing Union, while aligning with the Bank for International Settlements’ reflections on a global platform for improving international payments.

Supervision

The integration of capital markets would also be greatly enhanced by genuinely European supervision, along the lines of the US SEC or the European Single Supervisory Mechanism for banks. In this way ESMA49 could exercise joint oversight, along with national authorities, over cross-border players that have acquired systemic importance, including certain market infrastructures: CCPs and central securities depositories (also involving the ECB for the latter). This architecture is necessary to ensure greater consistency in the practices and decisions of the oversight authorities.

3.3 Public efficiency: a national and European medium-term fiscal strategy

The European – and especially the French – fiscal debate must now address two different albeit interdependent issues.

The first concerns deficit levels and future debt sustainability. This is the purpose of discussions around the Stability Pact. In early 2024, political agreement was reached on new EU fiscal rules. These remain too complex and, more specifically, they continue to adhere to a rather theoretical notion of structural deficit, without having replaced it with that of spending rules. However, they are trying to link fiscal adjustment, public investment and reforms. This common stability framework will make it possible to regain some room for manoeuvre. The main thing now is to actually apply it. This means that France, which is one of the countries with both high levels of public debt and a firmly negative fiscal balance (-5.5% of GDP in 2023, one of the worst performances in Europe), must finally adopt a credible fiscal strategy – and then stick to it (see box).

On this condition, and on this condition only will we be justified in pointing out to Germany that excessive fiscal virtue can turn into a mistake during the period of quasirecession it is currently experiencing. For many economists – including German economists – and for the Bundesbank itself, the constitutional “debt brake” (Schuldenbremse) is excessively rigid.50

The second issue, which unfortunately tends to be much less debated, is that of prioritising spending, and consequently its effectiveness. This is the key to cutting deficits. While the French challenge is especially daunting, it also illustrates a broader European challenge: how can we preserve what is most important in our shared social model – based on strong public services, social protection and tax redistribution – while at the same creating leeway for future additional spending? And this spending is likely to be significant, particularly for the climate, defence and the effects of an ageing population.

First and foremost, regarding operating expenditure, we need innovative public management together with explicit and sustainable priorities. Although more academic research is required in this area, certain types of expenditure have a more favourable effect on long-term economic growth and productive capacity.51 By making current and operating expenditure more efficient, governments will be able to prioritise public expenditure on the future: investment in education and skills, innovation and high valueadded industries (also related to the climate and digital transformations).

Subject to this better national discipline, Europe could and should arm itself with a common fiscal capacity. Whereas the EU budget has remained unchanged since its creation – both in its relatively modest amount (1% of EU GDP, excluding the NextGenerationEU programme (NGEU)) and its composition – the exogenous shocks that have occurred since 2020 have demonstrated the need to provide common solutions to common challenges. These solutions have taken the form of temporary programmes outside of the multiannual financial framework, the most emblematic of which was the EUR 750 billion NGEU programme of 2020. In view of the structural transformations that need to be achieved at European level, these collective solutions could be extended on a permanent basis through a common fiscal capacity, by giving priority to European public goods.52

Europe and France currently have doubts about their economic future. Barely two years after the pandemic, the return of war to Europe in 2022 has created an anxietyprovoking energy and inflation crisis, but one to which the public authorities have responded effectively. Following on from the fiscal shields, central banks have made a major contribution to reducing inflation, and the Eurosystem is committed to bringing it back to its 2% target by 2025.

Now that we Europeans are emerging from the inflationary emergency, we must undertake structural transformations that have been put off for too long. France and Europe need an economic direction and a longer-term ambition. We need to make a success of the three transformations – work, digital and the climate. The democratic debate and the upcoming European elections must provide an opportunity to devise broadly shared solutions.

This Letter provides some economic insight as well as grounds for hope. Since its creation 25 years ago, the euro has proved a success in terms of the protection is offers and its galvanising effect. So let us stop this lamenting, self-flagellation and every man for himself: in no way do these drive economic growth. It is time for Europe to come together to leverage its economic strengths to the full: its size (a single market that is as big as – and therefore needs to be as attractive as – the American market), multiplied by the financial firepower of our savings, and by greater public efficiency. In a more fragmented and tougher world undergoing profound transformation, Europe has effective levers at its disposal. Our economic destiny is largely in our own hands, and minds. This conviction should be the mainstay of our confidence. To paraphrase Raymond Aron, we can believe in the success of the European economy, but on one condition: that we have the will to be successful.53

Avenues for consolidating french public finances

The symptoms of “France’s fiscal malaise” are well-known and longstanding (see section 2.1): the accumulation of large deficits over more than 40 years (5.5% of GDP in 2023, the largest in the euro area after Italy), leading to a steady rise in public debt to 111% of GDP today, 20 percentage points higher than the euro area average and nearly 50 percentage points higher than Germany’s deficit. Correcting this deterioration is now imperative to regain our fiscal sovereignty. Of course, the decision on which savings and revenue measures to introduce should be made by democratic debate – under the aegis of the government and Parliament – and not by the Banque de France. However, the central bank has a duty to inform this debate with its own comprehensive economic analysis, which comprises three main avenues.

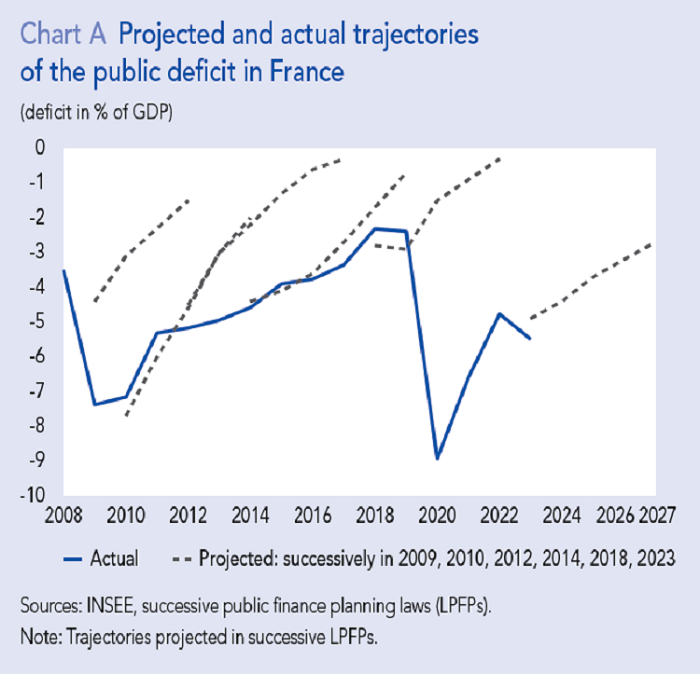

1. Face the truth and be credible from now on

For the past 15 years (since 2009), France has submitted multiyear fiscal plans as part of its public finance planning laws, which is a good thing. But for the past 15 years, through different majorities and governments, France has consistently failed to follow through on its commitments (see Chart A), seriously undermining its credibility in Europe. This has to change: forecasts – including for growth – need to be more realistic, and verified by the Haut Conseil des finances publiques (HCFP – High Council for Public Finances). They also need to be implemented much more rigorously and persistently. The new stability programme put forward by the government in April still raises questions: the general trajectory of a reduction in the deficit to below 3% of GDP in 2027, and a first, more realistic step of 5.1% in 2024, appear welcome; but details are needed on the measures to be implemented to achieve it, and the growth forecasts do not appear to take sufficient account of the restrictive impact of fiscal tightening.1

Another specifically French characteristic is the staggered and continuous rise in public debt: all countries have sharply increased their deficits in the face of the shocks (the financial crisis of 2009, the pandemic of 2020). But, unlike our neighbours, we fail to reduce them quickly enough when conditions improve. The recovery cycle, which is set to accelerate over 2025-26 (see section 1.2), together with the gradual easing of monetary policy, create a favourable context for structural fiscal consolidation: this will of course have a moderately restrictive impact on growth in the short run – which will depend on the qualitative composition of the savings – but this fear should not be overplayed to justify putting off the consolidation yet again.

2. Focus on spending first, with broadly spread and fair measures

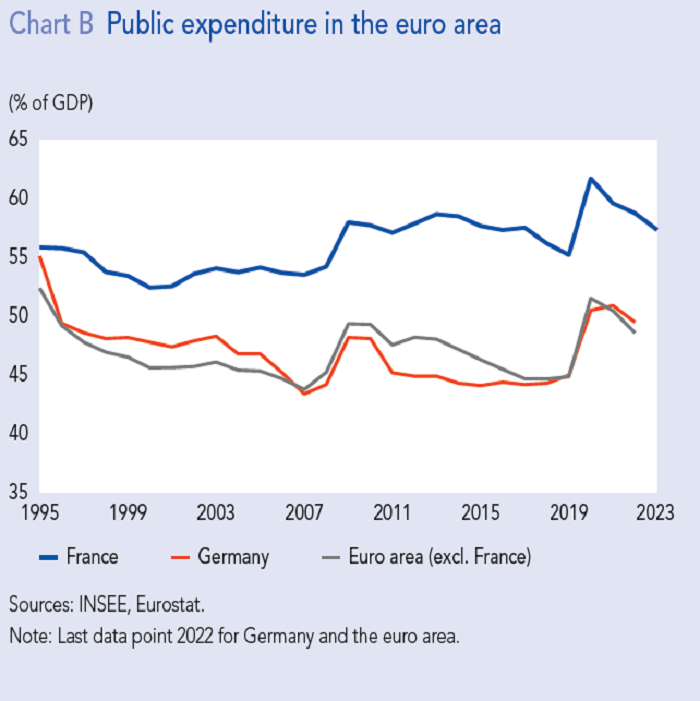

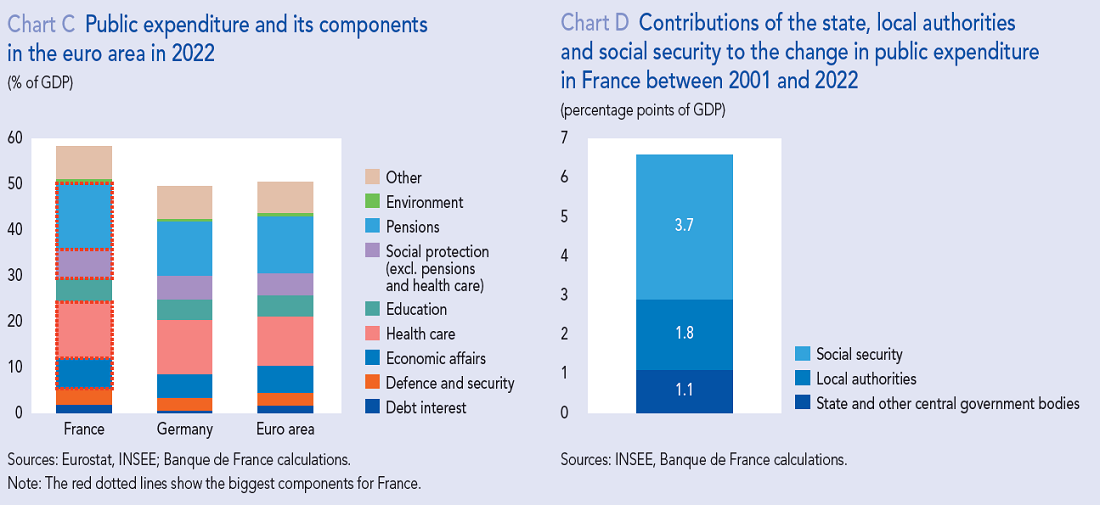

The deep-rooted cause of “France’s malaise” is the persistent growth in public expenditure. The European social model – consisting of strong public services, social protection and fiscal redistribution – has the legitimate support of the vast majority of citizens. The problem is that, for the past 30 years, there has been a widening gap between France’s public expenditure and that of its European neighbours, even though they share same social model. This “performance gap” has now reached 10 percentage points of GDP (58.8% of GDP in France in 2022 compared with an average of 48.6% for the euro area excluding France) (see Chart B).

The last few years have done nothing to reduce the gap: even after getting over the “bump” of exceptional support related to Covid and energy prices, our total public expenditure-to-GDP ratio is still higher than in 2019. In volume terms, excluding the effect of this exceptional expenditure, it could increase by more than 2% in 2024.2 Expecting this upward drift to be resolved solely by a future growth acceleration or a return to full employment is an illusion that has been entertained for too long.

It is high time, not to decree austerity and a general reduction in spending, but to achieve a quasi-stabilisation in volume terms. This assumes an effort in terms of priorities and efficiency that is fair and shared by everyone: not just the state, but local authorities and social services as well. It is notably in welfare spending – mainly pensions, but also health care and unemployment benefit – and at local government level – with a 50% rise in staff numbers – that the gap with our neighbours has widened most over the past two decades (see Charts C and D).

3. On taxes, at the very least stop cutting them, and maybe broaden certain tax bases

We are too quick to focus the debate on taxes, notably since the announcement of the poor deficit figures at the end of March, and in doing so, we tend to mistake the symptom (taxes) for the cause (expenditure). There is no realistic fiscal measure that can genuinely offset the expenditure overshoot. The fact remains that the successive tax cuts since 2014 have added to our deficits and today cost us around 2 percentage points of GDP. The first priority should therefore be to suspend any new, unfunded tax cuts, for businesses as well as households.

The size of the consolidation needed – which must now be more than the Cour des Comptes’ initial estimate3 of EUR 50 billion by 2027 – may mean passing measures to boost tax revenues, in addition to savings measures. This could be justified given the fall in the tax-to-GDP ratio in 2023: according to the stability programme, it is expected to remain at an average of 43.9% over the period 2024-27, significantly below its pre-Covid level (44.6% over the period 2015-19). Rather than raising tax rates, and in addition to the suggested “taxation of rents”, these targeted fiscal measures could – without taboos – be about broadening the tax base. This would also be fairer: for businesses, some tax breaks mainly benefit larger groups, while for households they mainly help the better off. Moreover, numerous tax deductions or exemptions are “brown taxation” or anti-green measures; and some reductions in social security contributions could be better targeted.

1 See opinion of the High Council for Public Finances, 16 April 2024.

2 As measured by the European Harmonised Index of Consumer Prices (HICP).

3 Final Eurostat estimates of 17 April 2024 and final INSEE estimates of 12 April 2024.

10 Use of the flexibility margin remains well below the limit of 20%, at 15.1% in the fourth quarter of 2023.

13 As for euro banknotes and coins, these were first put into general circulation at the start of 2002.

24 For example, for summarising, extracting and classifying data, or for generating computer code or text.

25 For example, carbon trading, a carbon tax, direct taxation of energy consumption.

34 The Digital Services Act of 19 October 2022 outlines a series of rules to make digital platforms more accountable and combat the distribution of illegal content. The Digital Markets Act of 14 September 2022 aims to prevent digital titans from abusing a dominant position and to offer European consumers greater choice.

47 For example, Scale-Up Europe (2021), or the European Tech Champions Initiative (ETCI, 2023) sponsored by the EIB with contributions from five EU Member States, including France.

48 SFDR, Sustainable Finance Disclosure Regulation, in the financial services sector; CSRD, Corporate Sustainability Reporting Directive.

49 European Securities and Markets Authority (ESMA), which is headquartered in Paris.

53 In 1939, Raymond Aron wrote: “I also believe in the final victory of democracies, but on one condition, that they want to be victorious”.

Download the PDF version of this document

Updated on the 25th of July 2024