Source

Data is provided by Issuer Paying Agents acting on behalf of issuers of commercial paper and medium-term notes. Information is collected on a security-by-security basis and encompasses the characteristics of the issues (ISIN code, currency, denomination, issue date, maturity date…) and of the corresponding transactions (type of transaction, amount, rate…). The Banque de France calculates and discloses aggregated information.

Scope of calculation

Calculation is based upon the whole set of data registered on the primary market, including:

- intra-group trades

- transactions with private clients of credit institutions

- transactions of non-resident issuers

The commercial paper and medium-term note Markets

For further details concerning the main features of commercial paper and medium-term note markets, you will find the necessary information on the following page: Commercial paper and medium-term note market

Volumes

The volume-related data refers to outstanding amounts, primary market issuances as well as redemptions. Issuer Paying Agents report data in the original currencies, which is converted into euro by the Banque de France, applying the end-of-day exchange rates for the reference day. The volumes are published at their corresponding value in EUR, unless otherwise stated.

Categories of issuers

The categories of issuers rely on the definitions of the institutional sectors given by the European System of Accounts, which constitute the framework for monetary statistics within the Eurosystem. However, the terminology chosen has been adapted to take into account specificities of the markets. The issuers, whether resident or not, are categorized as follows:

- bank issuers: credit institutions (of which mortgage credit institutions “sociétés de credit foncier”), funding companies “sociétés de financement” and the Caisse des Dépôts et Consignations;

- other financial issuers: insurance corporations, investment firms, financial auxiliaries and securitization vehicles;

- non-financial issuers: public and private non-financial corporations;

- public issuers: central and local government authorities, and social security funds (public agencies and regional hospital centers), international organizations.

Average issuance rates

Yield statistics are published only for euro-denominated commercial papers.

Average yield statistics, broken down by original maturity and program rating, are calculated on a weekly and monthly basis and available in the Average issuance rates by original maturity and rating review.

The rates are weighted by the nominal amount of the transactions. The trades included in the calculation are chosen according to the specifications listed in the table below:

|

Breakdown by ratings and original maturity Weekly and monthly statistical reviews |

|

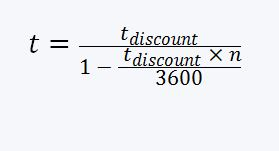

| RATES | Fixed money market rates and EONIA or €STR floating rates : rates codes : 001 and 003, 037 and 039, 047 and 049 |

| SPECIFIC CALCULATIONS |

Image

image

ti = spread + EONIA (overnight issuances)

ti = spread +EONIA-linked Overnight Indexed Swap (mid price) of the appropriate maturity, issuances over 1 day

ti = spread+€STR (overnight issuances)

ti = spread + EONIA-linked Overnight Interest Swap (mid price) of the appropriate maturity,-0,085 ( issuances over 1 day)

|

Confidentiality

Average rates are published only if at least three issuers are reported within any given breakdown by ratings and maturity.

Ratings

The issues are classified into 5 rating classes, on the basis of the rating programme:

Commercial papers

| STANDARD AND POOR’S | FITCH RATINGS | MOODY'S | DOMINION BOND RATING SERVICE | ETHIFINANCE | SCOPE RATINGS | ||

|

CLASS 1 |

A-1+ |

F1+ |

P-1 |

R-1Hi, R-1Mi |

|

S-1+ |

|

|

CLASS 2 |

A-1 |

F1 |

|

R-1Lo |

EF1+ |

S-1 |

|

|

CLASS 3 |

A-2 |

F2 |

P-2 |

R-2Hi, R-2Mi, R-2Lo |

EF1 |

S-2 |

|

|

CLASS 4 |

A-3, B, C, D |

F3, B, C, D |

P-3, NP |

R-3, R-4Sp, R-5Hs |

EF2, EF3, EF4, EF5, EFD |

S-3, S-4 |

|

|

UNRATED |

|

|

|

|

|

|

|

Medium term notes

| STANDARD AND POOR’S | FITCH RATINGS | MOODY'S | DOMINION BOND RATING SERVICE | ETHIFINANCE | SCOPE RATINGS | ||

|

CLASS 1 |

AAA |

AAA |

Aaa |

AAA |

AAA |

AAA |

|

|

CLASS 2 |

AA+, AA, AA- |

AA+, AA, AA- |

Aa1, Aa2, Aa3 |

AA Hi, AA, AA Lo |

AA+, AA, AA- |

AA+, AA, AA- |

|

|

CLASS 3 |

A+, A, A- |

A+, A, A- |

A1, A2, A3 |

A Hi, A, A Lo |

A+, A, A- |

A+, A, A- |

|

|

CLASS 4 |

BBB+, BBB, BBB-, BB+, BB, BB-, B+, B, B-, CCC+, CCC, CCC-, CC, D |

BBB+, BBB, BBB-, BB+, BB, BB-, B+, B, B-, CCC, CC, C, D |

Baa1, Baa2 Baa3, Ba1, Ba2, Ba3, B1, B2, B3, Caa1, Caa2, Caa3, Ca, C |

BBB Hi, BBB, BBB Lo, BB Hi, BB, BB Lo, B Hi, B, B Lo, CCC, CC, C, D |

BBB+, BBB, BBB-, BB+, BB, BB-, B+, B, B-, CCC+, CCC, CCC-, CC, C, D |

BBB+, BBB, BBB-, BB-, BB, BB-, B+, B, B-, CCC+, CCC, CCC-, CC, C, D, SD |

|

|

UNRATED |

|

|

|

|

|

|

|

If multiple ratings from different credit rating agencies are available, the lowest rating class prevails.

Maturity breakdowns

The maturity of issuances relates to the number of calendar days between the settlement date and the maturity date (redemption date).

| Maturities | Original maturity of issues (number of days) |

|---|---|

| 1 day | 1 day1 |

| 1 week | 7 +/- 2 days |

| 2 weeks | 14 +/- 2 days |

| 1 month | 30 +/- 7 days |

| 2 months | 60 +/- 10 days |

| 3 months | 90 +/- 10 days |

| 4 months | 120 +/- 10 days |

| 6 months | 180 +/- 10 days |

| 9 months | 270 +/- 10 days |

| 1 year | From 340 to 365 days (366 for leap years) |

1 Overnight issues (1 day maturity) include trades settled on Fridays, and redeemed on the following Monday.

Average weighted original and residual maturities

The original maturity of an issue is the number of days between the value date of the transaction (included) and the maturity date (excluded).

The residual maturity of an issue calculated on a date d is the number of days between d and the maturity date (excluded).

Average maturities are weighted by the volume of issues.

Release frequency

Statistical reports are released on a daily, weekly and monthly basis:

- Daily reviews are disclosed on the following business day;

- Weekly reviews are usually disclosed each Tuesday or Wednesday following the reference week;

- Monthly reviews are disclosed 4 or 5 business days after the end of the reference month.

Updated on the 22nd of November 2023